On April, 20th the EU finally passed its landmark Markets in Crypto-Assets (MiCA) regulation. Originally introduced in 2020 in response to a global stablecoin initiative, this is one of the first attempts to implement a comprehensive, cross-jurisdictional, and supervisory framework for crypto assets. MiCA is expected to come into force in 2024.

As with any regulation, the goals of MiCA include ensuring legal clarity, protecting investors and consumers, and defending market stability while promoting innovation. Moreover, MiCA hopes to alleviate the uncertainty which may stem from the continued fragmentation of the regulatory landscape.

MiCA clarifies that tokens defined as ‘financial instruments’ will be subject to:

Any business activity dealing with digital assets.

Interestingly, lending is not specifically referred to by MiCA. However, digital assets classified as financial instruments are governed by the existing regulations.

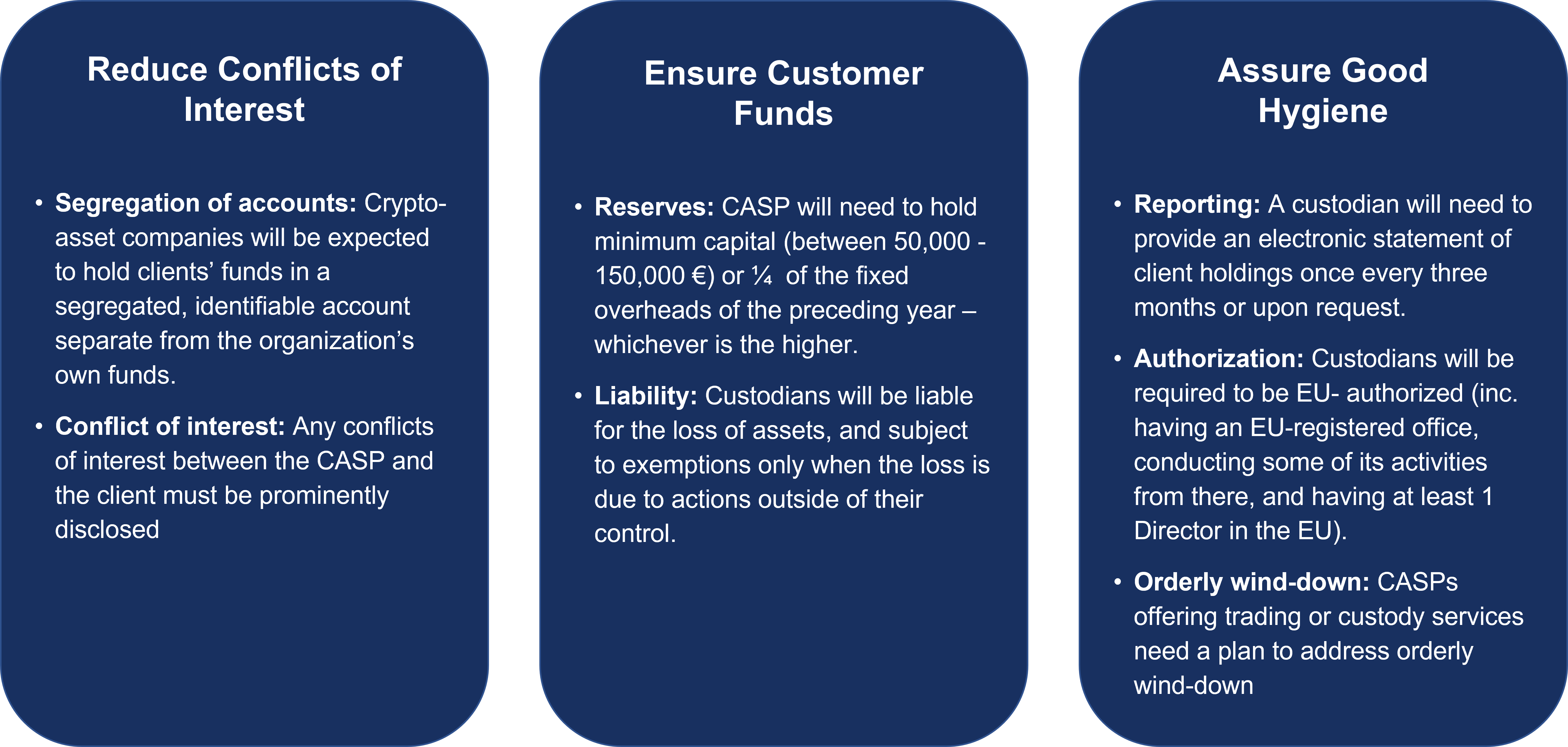

MiCA regulations, had they been in place prior to 2022, may very well have prevented at least some of the failures which plagued the industry in 2022. That said, pending ratification and enactment, MiCA will go a long way to reinstating trust and transparency in the digital asset sector. So what are some important takeaways for custodians and others operating in the digital asset services space? These can be broken down into 3 categories:

ART (asset-referenced tokens) and EMT (electronic money tokens) are subject to some additional requirements. One thing to note: Under MiCA, yield and interest are currently prohibited. For the sake of clarity, discounts, rewards, and compensation, are considered yield and interest.

How this relates, if at all, to staking remains to be seen. DeFi, for example, is not in scope for now. However, perhaps in the future.

NCAs (National Competent Authorities, such as BaFin in Germany for example) will be responsible for the enforcement of MiCA regulations. Their powers include, amongst other things, the ability to:

While MiCA does indeed attempt to provide a comprehensive framework, there remain additional regulations that will continue to affect the digital asset industry in EU. We’ve discussed some of them above:

MiCA, does indeed attempt to provide a holistic view of regulations in the digital asset sphere. For those jurisdictions without a comprehensive framework, MiCA can serve as a blueprint or comprehensive starting point. That said until MiCA is implemented and enacted, we have yet to see which loopholes remain. It is also likely that as the industry evolves, MiCA too will continue to evolve.

Importantly, all of these new rules and regulations will affect the policies and requirements of custody providers. Whether these are 3rd party custodians, or institutions opting for self-custody of their own digital assets. This makes choosing a custody solution for your institution, particularly crucial. Amongst the many aspects that you should look into is the flexibility of systems and workflows, but more on this in the last article of the series which drills down into the potential implications these new and evolving regulations have on choosing an institutional grade custody solution.

Stay tuned. In the meantime feel free to reach out to us with any questions, or learn more: www.gk8.io.